24-Apr-2025

Looking to buy a home in Illinois? One of the biggest obstacles is often the down payment—and with today’s incredibly high cost of living, saving up could feel a bit overwhelming.

But here’s the good news – in 2025, you may qualify for a no down payment loan Illinois program.

Thanks to an array of no-money-down mortgage options and down payment assistance in Illinois, buying a home has become more accessible than ever—whether you’re a first-time buyer, looking for a cozy spot in the suburbs or settling into a small town.

Explore your options for a zero down payment loan in Illinois and check out our comprehensive guide to down payment assistance to witness how you can qualify.

Your path to homeownership begins here and now –

The program of no down payment loan Illinois enables buyers to buy a home without putting money down, usually through 100% substantial or financing programs.

In Illinois, all these options are widely available through federal programs including VA and USDA loans, along with country and state level assistance. This assistance can significantly lower or eliminate the down payment.

Below, we have broken down every option – covering eligibility criteria, advantages, and major considerations.

A USDA loan could be your golden ticket to homeownership—especially if you’re looking to buy in a rural area of Illinois. The best thing? No down payment is required.

Provided through the Rural Development program of the U.S. Department of Agriculture, USDA loans offer up to 100% financing, making them a perfect choice for buyers looking for a zero down payment loan in Illinois.

Why it stands out –

Backed by a USDA loan, you can easily finance the entire purchase price—and even roll in prepaids or closing costs. Seller concessions are also allowed that means you could potentially move in without spending even a single penny!

Who’s eligible –

To qualify, the home should be in an eligible rural area. There are also certain limitations on household income to ensure that these loans benefit moderate to low-income families. You can check eligibility online via the USDA’s tool.

Keep in mind –

These loans are location-centric, so if you’re shopping in suburban or urban areas, this might not be the ideal fit. Also, income caps could rule out higher earners. While Illinois provides property tax perks such as a whopping $6,000 homestead exemption, especially for primary residences, it’s separate from the loan perks.

For those who fail to qualify for a USDA loan, don’t bother—there are still variety of options available through mortgage down payment assistance Illinois programs, which can help lower or even eliminate upfront costs.

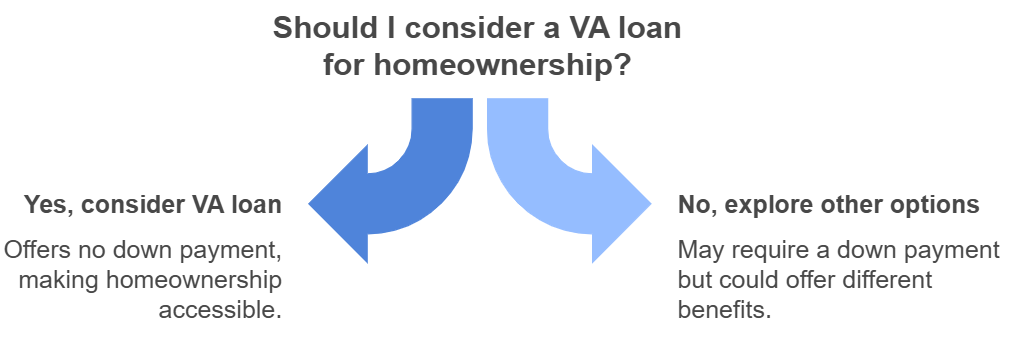

Are you a veteran? Or, serving in the military at present? If yes, then keep in mind that a VA loan could be your ultimate path to homeownership—with absolutely no down payment required.

Provided by the Department of Veterans Affairs, this program is a highly valuable option for no down payment loan Illinois for those who have served.

Why it stands out –

VA loans provide up to 100% financing, which means that you can buy a home anywhere in Illinois without putting even a single penny down. These loans can also be combined with down payment assistance programs like those provided by IHDA to help lower other upfront costs.

Who qualifies

VA loans are widely available to active-duty service members, eligible veterans, and certain members of the National Reserves or Guard. There are some specific service requirements, so it’s crucial to check eligibility with a VA-approved lender to determine whether you qualify.

Things to consider

Since this loan is tailored especially for military personnel, it’s not available to civilian buyers. Interest rates and terms might differ slightly by lender, but the benefit of zero down payment is a major perk for those who qualify.

If you are eligible, a VA loan can make buying a house in Illinois a lot more affordable and within reach—without any stress of saving for a large down payment. Don’t forget to check eligibility.

While IHDA programs don’t provide true no-down payment loans, they offer substantial assistance that can significantly lower your out-of-pocket cost to as little as around $1,000 or up to 1% of the purchase price—effectively making them near-zero down payment option for many Illinois-based homebuyers.

IHDA provides 3 main programs to support homebuyers, each offering different kinds of repayment and assistance terms. These options can help make a home feel within reach—even for those looking for a no down payment loan Illinois solution, as detailed in the chart below –

| Program Name | Assistance Amount | Type of Assistance | Repayment Terms | Mortgage Details | Eligibility Requirements |

| Access Forgivable | Around 4% of purchase price, up to $6,000 | Gift, forgiven monthly over 10 years | Zero repayment required | 30-year, fixed rate, affordable interest | Credit score ≥640, $1,000 or up to 1% contribution, primary residence, homeownership counseling, every Illinois county, first-time/repeat buyers |

| Access Deferred | Around 5% of purchase price, up to $7,500 | Interest-free loan, deferred for life | Repaid while refinancing, selling, or paying off mortgage | 30-year, fixed rate, affordable interest | Same as above |

| Access Repayable | Around 10% of purchase price, up to $10,000 | Interest-free loan | Repaid monthly over 10 years | 30-year, fixed rate, affordable interest | Same as above |

These programs have compatibility with an array of mortgage types—including FHA loans in Illinois, VA, USDA, FHLMC HFA Advantage, and FNMA HFA Preferred—offering homebuyers unmatched flexibility. Around 10% of first-time homebuyers in Illinois benefit from IHDA products, reflecting their growing popularity.

Initiatives such as SmartBuy and Opening Doors are specifically tailored to boost access to homeownership, especially for underrepresented communities.

A modest contribution is needed—typically $1,000 or up to 1% of the purchase price—and borrowers should meet income as well as purchase price limits, along with a nominal credit score of 640. Homeownership counseling is also non-negotiable, and while extremely advantageous, might be a serious obstacle for some applicants.

Beyond federal and state options, several Illinois counties provide localized down payment assistance to lift the financial burden off the homebuyers.

Provides up to $5,000 for closing costs and down payment. Requirements include –

Offers around $5,000 as a 5-year forgivable loan with similar criteria:

Important Note – These programs are geographically restricted and might include additional local needs like participation in community development initiatives.

For Illinois-based residents looking for no down payment loans, USDA loans are perfect for rural areas, while VA loans provide eligibility to military personnel. Every option has unique eligibility criteria, so it’s crucial to consider factors such as income, location, and credit score.

For further details related to application, and to check eligibility, explore the linked resources or connect to your local housing authority for more personalized guidance.