11-Jul-2025

Owning a house is one of the most crucial and challenging financial milestones in a person’s life. For the citizens of the U.S., this journey is not only about creating equity and building stability – it also brings a wide range of tax benefits. If you have opted for a home loan (Indiana or Illinois) or are looking to do so, gaining an understanding of the tax advantages available can help you reduce your financial burden significantly.

In our blog today, we will break down the extent of tax benefits you can get from a home loan in the USA, what matches the eligibility criteria, and how you can reap these rewards.

1. Mortgage Interest Deduction

What is it?

One of the most important tax benefits of a home loan is the deduction of mortgage. Homeowners can decrease the interest paid on a mortgage used to purchase, build, or boost their primary residence (or second home).

How much can you claim?

Example –

If you have a mortgage of around $500,000 and paid $20,000 in interest over the year, you might be able to subtract the entire $20,000 from your taxable income.

Important Note: You are required to itemize deductions on Schedule A of your federal tax return (Form 1040) for claiming this.

2. Property Tax Deduction

What is it?

Homeowners can also claim local and state property taxes they pay on their real estate.

Deduction Limit:

As of 2024, you can easily deduct up to $10,000 total for local and state taxes (including property tax as well as income/sales tax). This is called the SALT cap.

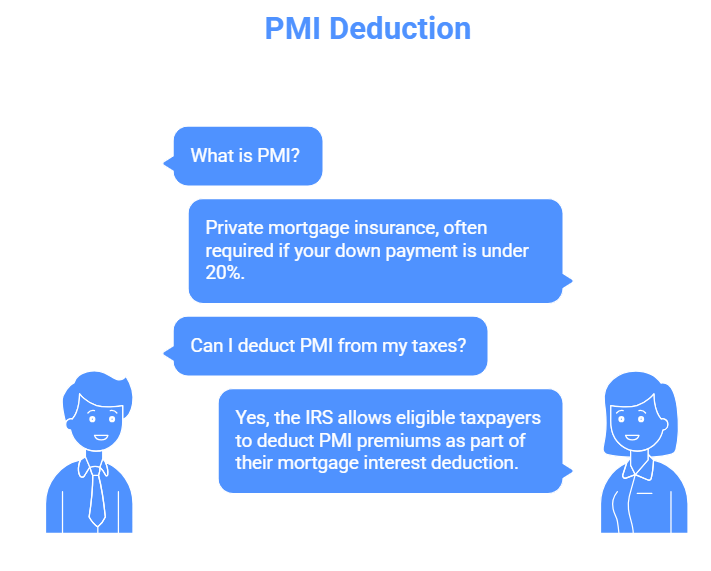

3. Mortgage Insurance Premium Deduction

If your down payment was under 20%, you likely pay PMI (private mortgage insurance). The IRS enables eligible taxpayers to write off PMI premiums as an integral part of their mortgage interest deduction.

Qualifications:

4. Mortgage Points Deduction

When you obtain a mortgage, you may pay upfront charges to to decrease your interest rate (also referred to as “buying down the rate”). These points are deemed as prepaid interest and may be deductible.

Rules:

5. Home Equity Loan Interest Deduction

The interest on a HELOC (home equity loan or line of credit) is deductible only if the funds are used to purchase, build, or substantially enhance the home.

Not eligible:

If the home equity loan is allocated to pay off credit card debt or cover a vacation, the interest can’t be claimed.

6. Itemized Deduction vs. Standard Deduction

Prior to claiming your tax benefits from a home loan, you’ll have to determine whether to itemize your deduction or take the standard deduction.

Standard Deduction (2024):

You should just itemize (and claim house loan deductions) in case the total of your itemized deductions goes beyond the standard deduction amount.

Some Additional Notes

Even though the actual tax credit program expired in 2010, Congress periodically launches new homebuyer tax incentives.

While not closely linked with your mortgage, if you decide to transfer ownership of your house, you could shield up to approximately $250,000 ($500,000 for couples) in gains from taxes – given it was your principal residence for at least 2 of the past 5 years.

| Tax Benefit | Deduction Limit | Key Condition |

| Mortgage Interest | Up to $750,000 mortgage | Should itemize deductions |

| Property Taxes | $10,000 SALT cap | Local and state taxes combined |

| PMI Premium | Income under $109,000 | Deductible as mortgage interest |

| Mortgage Points | Full amount paid | Should meet IRS criteria |

| HELOC Interest | Varies | Funds should improve the home |

Final Words: Are Home Loans Tax-Friendly?

Yes, absolutely! Although the Tax Cuts and Jobs Act of 2017 placed certain restrictions on some deductions, U.S. homeowners can still access different tax-saving opportunities. The key is to clearly understand which expenses qualify, if itemizing makes sense, and how recent changes in tax law affect your eligibility.

If you’re still uncertain, consider consulting a CPA or tax advisor. Taking adequate time to understand your options can help you access thousands of dollars in tax benefits over the life of your mortgage.

Have any questions?

Looking to buy a home, or are you already a homeowner? Now is the ideal time to revisit your overall tax strategy. Gain an understanding of the importance of your home loan in your financial life – and make your house an asset during the tax season.