09-Apr-2025

The FHA loans in Illinois are tailored to facilitate homeownership, especially for first-time buyers and those with moderate incomes.

The following analysis, dated April 8, 2025, provides a comprehensive review of FHA loan limits, eligibility requirements, and down payment assistance in Illinois, offering potential beneficiaries a clear and in-depth understanding.

FHA loans in Illinois, insured by the FHA (Federal Housing Administration) through the U.S. Department of HUD (Housing and Urban Development), were introduced in 1934 to guide and assist borrowers with less-than-perfect credit.

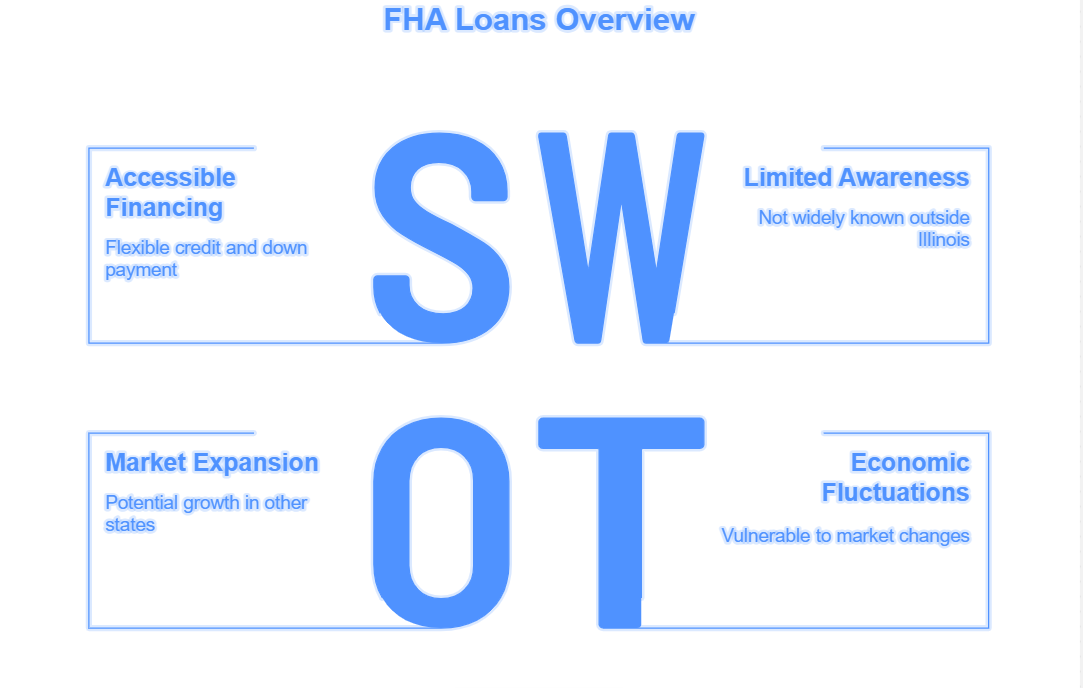

These loans are hugely popular, especially in Illinois, where the median home sale price reached around $280,000 in December 2024, as per New American Funding. With lower flexible credit guidelines and down payment requirements, FHA loans are an excellent option for everyone looking to buy a home for the first time and those who have difficulty making large down payments.

Check eligibility to see if an FHA loan is the suitable choice for you!

In 2025, the limits pertaining to FHA Loans in Illinois, are consistent across 102 countries, reflecting the housing market of the state. Set by HUD, and updated annually as per the NHA (National Housing Act) and FHFA (Federal Housing Finance Agency) conforming loan limits, the FHA loan restrictions for Illinois are as follows –

Each of these figures is verified by reliable sources like LendingTree and FHA.com, enabling borrowers to finance properties up to these amounts, with zero county-specific variations, unlike in a few states with high-cost areas.

Requirements pertaining to FHA Loans in Illinois perfectly align with national guidelines but bring flexibility for borrowers. Some of the major criteria include the followings –

Check eligibility to see if an FHA loan is the best choice for you!

The IHDA (Illinois Housing Development Authority) provides several DPA (down payment assistance) programs to boost FHA loan accessibility, as detailed on the IHDA website. Each of these programs, available to both repeat and first-time homebuyers, can be combined with FHA loans:

As noted by United Home Loans, these programs need a nominal borrower contribution (e.g., $1,000 or 1% of the purchase price) and a strict adherence to purchase price limits and income, bringing more affordability to homeownership in the housing market of Illinois.

To help you in decision-making, we present a chart that summarizes the advantages and drawbacks of FHA loans in Illinois, taking their integration with IHDA programs into consideration –

| Aspect | Pros | Cons |

| Down Payment | As low as a 3.5% with 580+ credit score, aided by IHDA DPA up to $10,000 | Requires mortgage insurance for the life of loan unless refinanced |

| Credit Flexibility | Accepts scores as low as 500, ideal for those with past credit issues | Lenders may have overlays, requiring higher scores (e.g., 620) |

| Loan Limits | High limit of $524,225 for single-family, covers most Illinois homes | Caps at $1,008,300 for four units might limit high-cost area purchases |

| IHDA Assistance | Forgivable, deferred, or repayable options, no interest on assistance | Income and purchase limits, geographic restrictions for some programs |

| Application Process | Straightforward with FHA-approved lenders, pre-approval available | Requires property to meet FHA standards, potential additional costs |

The process of applying for an FHA loan Illinois mirrors the national process but revolves around working with FHA-approved lenders like those listed on New American Funding. Some important steps include the followings –

While relying on IHDA assistance, it is crucial to work with an IHDA-approved lender to guarantee compliance with the program’s specific guidelines, as outlined on the IHDA website.

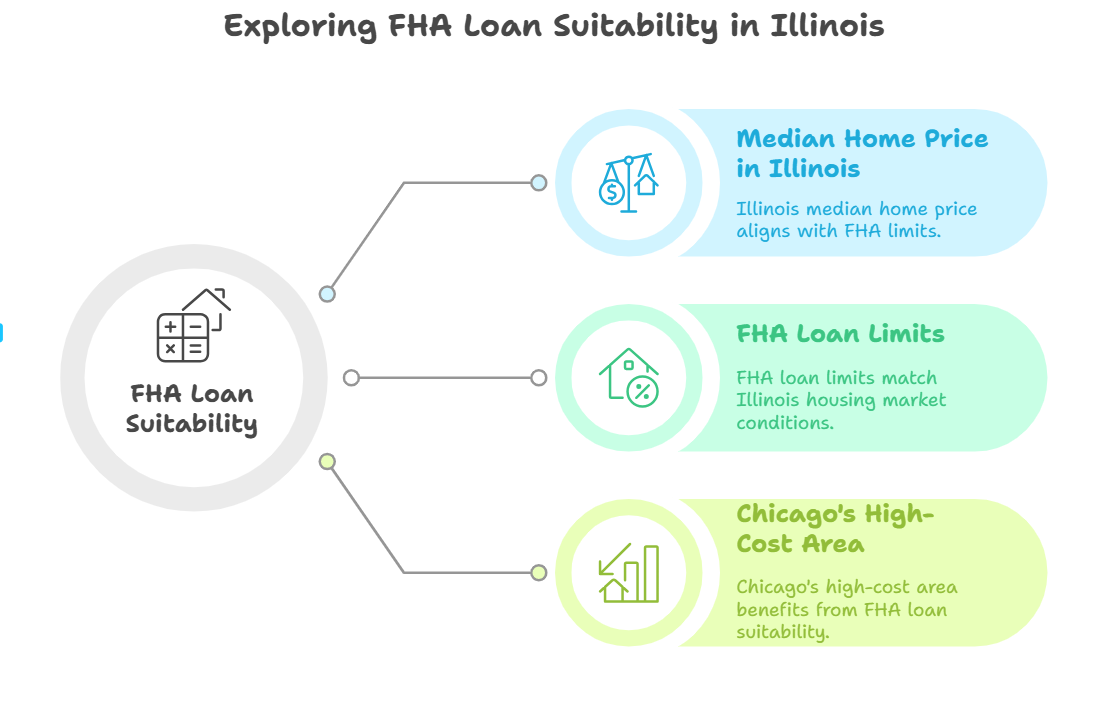

The median home price in Illinois (around $280,000 in December 2024) aligns perfectly with FHA loan limits, making them suitable for most buyers, especially in high-cost areas such as Chicago, where median prices reach up to $441,000 in counties like Cook, as per Madison Mortgage Guys.

Additionally, FHA loans allow gift funds for down payments, providing optimum flexibility that might surprise buyers anticipating stricter rules, as noted by Neighborhood Loans. Funding for IHDA programs might differ, with around 69% availability as of January 2025, per Down Payment Resource, leading to waiting lists. Buyers are required to confirm current terms with lenders, as program details and rates can alter.

FHA loans in Illinois, with flexible qualifications and uniform limits, offer a strong path to homeownership. When combined with IHDA assistance programs, they can cater to both repeat and first-time buyers. Borrowers must consult FHA-approved lenders for updated details to perfectly align with their market conditions and financial goals.