03-Jul-2025

Buying your very first house is indeed an amazing milestone, but before you embark on house hunting, it’s crucial to understand if you meet all the qualifying factors for the first time home buyer. Getting prepared can always help you access grants, reduced interest rates, and better loan programs. In our blog, we’ll unlock what it means to be a first-time buyer, some key credit and financial requirements, and property eligibility rules – additionally some effective tips to enhance your application.

Don’t forget to check eligibility prior to getting ahead with your homeownership journey.

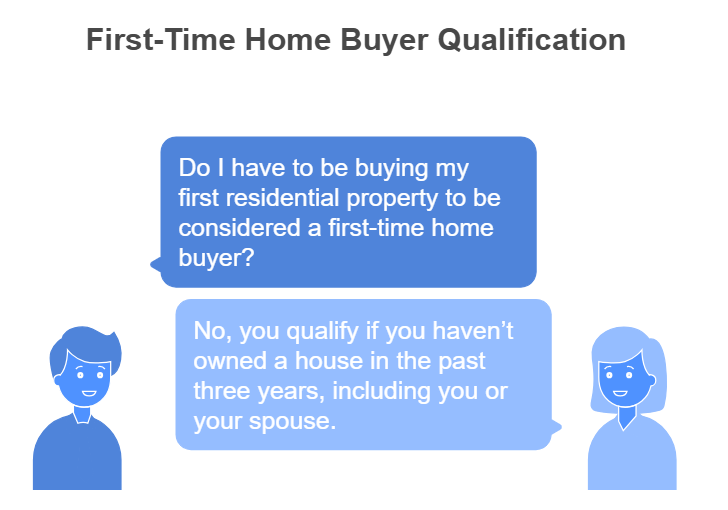

No, you don’t have to be buying your first residential property ever to be recognized as a first-time home buyer. As per the U.S. Department of HUD (Housing and Urban Development), you qualify in case you haven’t owned a house in the past three years. This includes your name as well as your spouse’s, in case applicable.

Also, there are certain exceptions. For instance, a single parent who once owned a house with a former spouse, or a homemaker who lost housing because of separation but shared the title, might still qualify.

Don’t forget to check eligibility in case you fall into one of these categories.

The discussion around qualifying factors for the first time home buyer will be incomplete without mentioning your credit score. While requirements differ depending on different types of loan, below are mentioned the general benchmarks –

A higher credit score could get you lower monthly payments and better interest rates. However, lenders also consider your credit history such as credit utilization and timely payments not just the number.

Ensure that you check eligibility by thoroughly reviewing your credit report and fixing any errors.

Lenders want to make sure that you have a reliable income. Most prefer at least 2 years of steady employment within the same industry. Documents that might be requested include –

Self-employed borrowers are required to provide additional documents like profit/loss statements as well as business tax filings. Provable and consistency income are key to enhancing your case.

Don’t forget to check eligibility in case your income has remained stable over the past 24 months.

Your DTI ratio refers to the percentage of your total pre-tax income that goes toward paying debts. This includes student loans, rent, credit card minimums, car loans, and the new mortgage payment.

Most of the first-time buyer programs prioritize a DTI ratio of around 43% or lower. Here’s how things are calculated –

DTI = (Monthly debt payments ÷ Gross monthly income) × 100

If your Debt-to-Income is way too high, you might be denied or provided less favorable terms. Paying off smaller debts or enhancing your income can help improve your ratio. Make sure that you check eligibility by calculating your DTI prior to applying.

One of the main advantages of being a first-time buyer is qualifying for lower down payment options:

However, you’ll still require funds for closing costs, emergency savings, and moving expenses. Keeping 2–3 months’ worth of funds on hand can boost your application. Don’t forget to check eligibility depending on how much you’ve saved.

Many down payment assistance programs need a completion of a first-time homebuyer education course. All these classes – available digitally or in person – cover topics such as –

They’re typically low-cost or free and take only a few hours to complete. Although not mandatory, these programs provide useful and genuine insights for new home buyers. Ensure that you check eligibility with your lender or local housing agency.

Some financing options don’t just review your qualifications, but they also inspect the property. For example –

Before submitting a bid, confirm that the home has the eligibility for your financing option. Check eligibility of both you as well as the property with your loan provider.

Understanding the qualifying factors for the first time buyer is important before you begin house hunting. Your income stability, DTI ratio, credit score, and savings all have vital roles to play. With certain preparation – and potentially the assistance of buyer education programs – you can maximize your chances of approval.

Check your eligibility today and take the leap toward buying your dream home.

Yes, absolutely! If you haven’t had a house in the past 3 years, most of the programs still consider you a first-time home buyer.

Low debt helps, but most lenders still need minimum credit scores. Consider credit-building steps such as secured cards or paying in a timely manner for several months.

Not all, but several state-backed loans and down payment assistance programs need a short education course. It’s a brief time commitment with enduring benefit.